Most budgets fail for a simple reason: they are too detailed to maintain. Twenty categories, receipts to sort, and by week three the spreadsheet is abandoned. The 50/30/20 rule survives because it asks only one question: of the money that comes in, how much goes to needs, how much to wants, and how much to savings?

This article explains how the rule works, when the percentages should bend, and how to run it with nothing more than your existing accounts. It is educational material, not personalized financial advice.

What the three buckets mean

The rule, popularized by Senator Elizabeth Warren and Amelia Warren Tyagi in All Your Worth, splits after-tax income three ways:

| Bucket | Target | What goes in |

|---|---|---|

| Needs | ~50% | Rent or mortgage, groceries, utilities, transport to work, insurance, minimum debt payments |

| Wants | ~30% | Dining out, streaming and subscriptions, hobbies, travel, upgrades you could live without |

| Savings | ~20% | Emergency fund, named goals, retirement contributions, debt payments above the minimum |

The line between a need and a want is personal, but there is a useful test: if losing it next month would threaten your housing, health, work, or legal obligations, it is a need. Everything else — however much you enjoy it — is a want.

A concrete example

Suppose your after-tax income is $2,000 per month. The rule suggests:

- $1,000 for needs

- $600 for wants

- $400 for savings and extra debt payments

Now compare that with what actually happened last month. Most people have never seen their spending grouped this way, and the first pass is usually a surprise: needs near 60%, wants near 35%, savings whatever is left — often close to zero. That gap between target and reality is not a failure. It is the information the budget exists to produce.

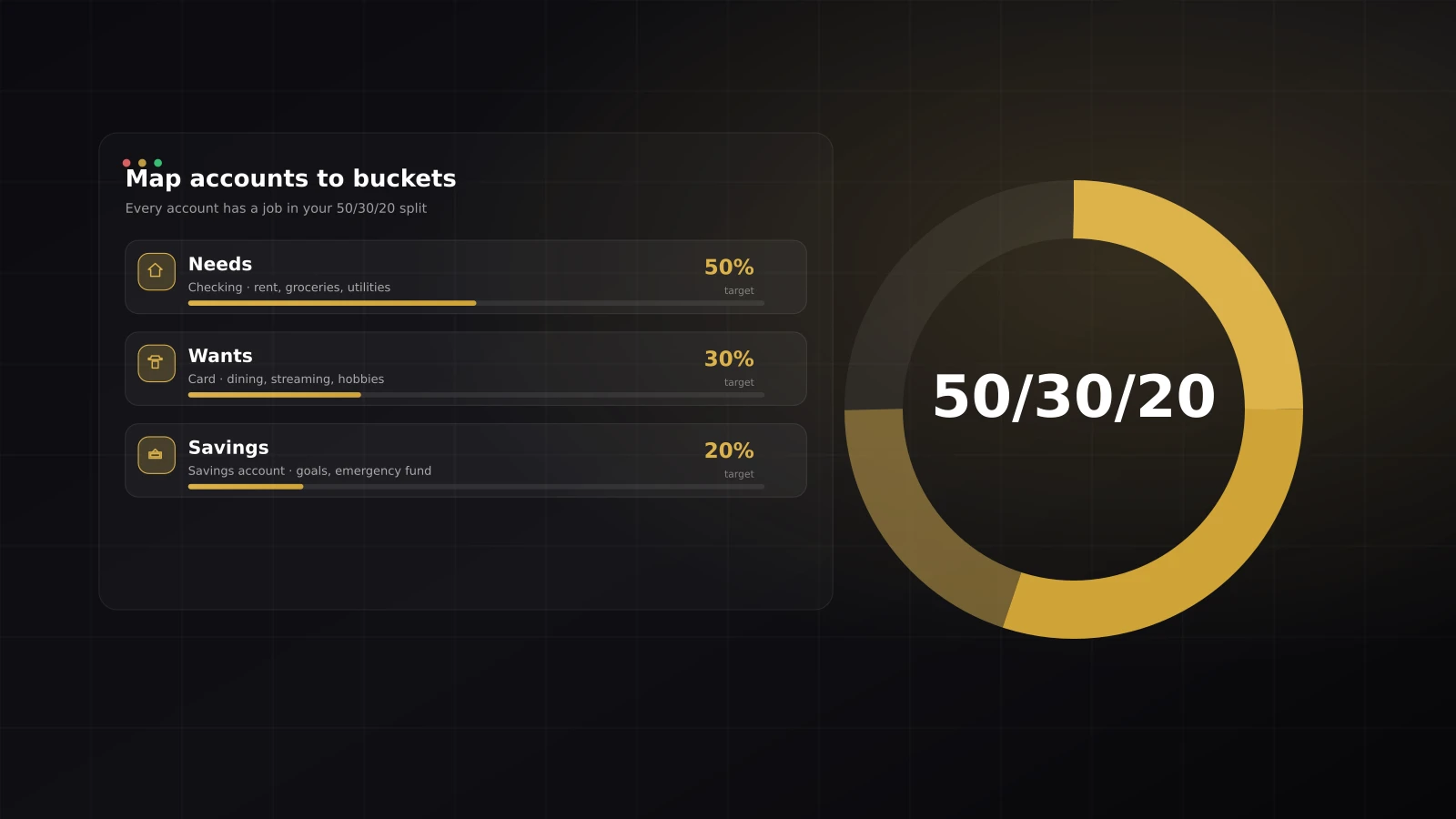

Map buckets to accounts, not categories

The most durable way to run 50/30/20 is to give each bucket a real account:

1. Needs live in your main checking account. Rent, utilities, and groceries come out of one place, so the balance itself tells you how the month is going.

2. Wants live on one card or one account. When dining out, streaming, and hobby spending share a single surface, “how much did I spend on wants?” stops being an archaeology project — it is one number.

3. Savings leave on payday. Transfer the 20% out the day income arrives, into a separate savings account. Money that never sits in checking never gets spent by accident. If you want the long-term math behind this habit, see how compound interest works.

This account-based version has a quiet advantage: it works even in weeks when you track nothing at all. The structure does the sorting.

When the percentages should bend

The rule is a compass, not a contract. Common, legitimate adjustments:

- High-rent cities. If housing alone takes 40%, needs may sit at 60% for a season. Shrink wants first, protect at least some automatic saving, and treat the imbalance as a known number rather than a vague worry.

- Aggressive debt payoff. Someone attacking a credit card balance might run 50/20/30 — cutting wants to 20% and directing 30% at the debt. The companion article on credit card APR and payoff basics explains why the interest math rewards this.

- Variable income. Freelancers should apply the split to a baseline month (their lowest typical income). Extra income in good months goes to savings first, which smooths the lean months.

The failure mode to avoid is silent drift: percentages that moved without a decision. Bending the rule on purpose is budgeting; discovering in December that wants averaged 45% is not.

A monthly review that takes ten minutes

At the end of each month, answer three questions:

- What did each bucket actually take? Three percentages, not thirty categories.

- Which single want grew the most? One honest answer beats a full audit. Recurring charges are the usual suspect — a quick subscription audit often frees several percentage points on its own.

- Did the savings transfer happen? If not, schedule it for payday next month so it cannot be skipped.

That is the whole ritual. Ten minutes, three numbers, one adjustment.

Where LucasApp fits

LucasApp tracks accounts, spending, and transfers in one place, so the three buckets stop being estimates. Group your accounts by job — needs, wants, savings — and the period summary shows what each one actually took this month. Lucas AI turns receipts and vouchers into recorded movements, which keeps the wants bucket honest without manual data entry.

Sources and further reading

- Consumer Financial Protection Bureau — Creating a budget

- Investopedia — The 50/30/20 rule (general reference)

Percentages and examples in this article are illustrations, not personalized advice. Adapt them to your income, obligations, and goals.

Frequently asked questions

What is the 50/30/20 rule?

A budgeting guideline that splits after-tax income into three buckets: about 50% for needs (rent, groceries, utilities), 30% for wants (dining out, streaming, hobbies), and 20% for savings or extra debt payments.

Should the percentages be exact?

No. They are a starting point, not a law. In cities with high rent, needs can exceed 50% for a while. The value of the rule is making the three buckets visible so you can move them deliberately.

Does the 20% include debt payments?

Minimum payments on debt count as needs because they are obligations. Anything you pay above the minimum works like savings — it reduces future interest — so it belongs in the 20% bucket.

What if my income changes every month?

Budget on your lowest typical month, not your best one. In good months, keep the needs and wants amounts stable and send the extra to the savings bucket first.